Journal of Women's Health Care

Open Access

ISSN: 2167-0420

ISSN: 2167-0420

Research Article - (2021)Volume 10, Issue 4

Recently in Ethiopia, there is an increasing movement to implement community based mostly insurance theme as integral a part of health care finance and significant movements has resulted within the unfold of the theme in several elements of the country. Despite such increasing effort, recent empirical proof shows entering have remained low. The aim of this study is to spot determinants of enrollment in community based mostly insurance implementation in South Gondar Zone, Amhara region

A community based mostly cross sectional survey was conducted to gather information from 1,035 family heads employing a multi-stag sampling technique. A binary logistic regression was accustomed to determine the determinants of family decisions for CBHI enrollment.

Out of the participants, (68.17%) were CBHI members. Besides, family size (AOR=2.18; CI=1.13-1.45), average health status (AOR=.590; CI=.281-.906), chronic malady (AOR=4.42; CI=1.92-8.22), theme benefit package adequacy (AOR=3.18; CI=1.90- 6.20), perceived health service quality (AOR=4.69; CI=1.78-7.70), CBHI awareness (AOR=4.78; CI=1.75-15.7), community commonality (AOR = 4.87; CI = 2.06–6.93) and wealth (AOR = 4.52; CI = 1.78–7.94) were vital determinant factors for entering within the community based mostly insurance theme.

CBHI awareness, family health condition, community commonality, quality of health service of health organizations and wealth were major factors that almost all confirm the family decisions to register within the system. Therefore, in depth and continuous awareness creation programs on the scheme; stratified premium – supported economic status of households; incorporation of social capital factors, notably building community commonality within the theme implementation are important to boost continuous enrollment. As perceived family health status and therefore the existence of chronic malady were also found vital determinants of enrollment, the government may need to seem for choices to create the theme obligatory.

Community, Health insurance, Enrollment, Determinants

AOR: Adjusted Odds Ratio; CBHI: Community Based Health Insurance; CI: Confidence Interval; COR: Crude Odds Ratio; OOP: Out of Pocket; UHC: Universal Health Coverage; EDHS:Ethiopian Demographic and Health Survey

Over the past two decades, many low-income and middle-income countries (LMICs) have found it progressively more difficult to maintain sufficient financing for healthcare services in an equitable [1].This distressing scenario triggered WHO and other international body to propose an alternative approach in the late 1990s; thereby, various forms of community based health care financing have been emerged [2]. Community based Health insurance (CBHI) schemes are classically risk-pooling approach that tries to spread health costs across households with different health profiles to ensure better access and enables cross subsidies from rich to poor populations. In June 2018, the Government of Ethiopia rolled out a pilot basis CBHI scheme in 13 Woredas of Amhara, Oromia, Southern Nations Nationalities and Peoples (SNNP), and Tigray regional states. Since its establishment, there has been increasing movement to support and spread pilot schemes in different parts of the country. For instance, by the end of June 2017, the number of scheme has grown in to 377 pilot Woredas [3].

Despite increasing support and spread of CBHI as noted before, recent empirical evidence shows enrolment has remained low across the scheme in being implemented areas indicating that CBHI has continued to fail to reach satisfactory levels of participation amongst targeted population [4]. As of June 2019 the federal ministry of health (FMOH) annual report shows, the overall enrollment rate in the pilot scheme was 55.5% [5].

One possible explanation for low scheme uptake is that, household or individual level characteristics combined with how one perceives CBHI scheme in the dimension of its effectiveness in meeting health care needs; quality of care; trust and provider competency [6]. As it was reported from the endowment effect and status quo bias complicated for individuals the decision to insure particularly in areas where insurance is a new concept and illiteracy rates are high, availability of health care facilities; episode of chronic illness in the household and an understanding of the product[7,8].

Furthermore, scheme related factors such as affordability; benefit packages and payment mechanisms also affect scheme uptake. However uptake of the Ethiopian CBHI program reveals the opposite, with the poorest quintile providing the largest share of CBHI beneficiaries and there is general agreement that the defined benefit package is adequate [9]. While there are concerns about scheme uptake and suggested factors to the problem, scientific evaluation of the factors affecting the decision to enroll in CBHI the scheme in being implemented areas are still very scarce. As to the researcher knowledge, in Ethiopia a few studies were conducted on subjects related to CBHI which mainly focused on factors affecting willingness to join and impact of CBHI and scheme performance [10-12].

Currently, Ethiopia has begun establishing a comprehensive and sustainable risk protection system with health care financing mechanisms adapted to our country’s needs so as to improving financial access to health care services; improving quality of health care service and increase resource mobilization in the health sector through CBHI. However, the objective is, there is little attention has been paid to understand factors affecting uptake of CBHI; this can partly be attributed low enrollment in CBHI. Therefore, the subject should be studied and it provides information on factors affecting uptake of CBHI so as to design interventions to increase scheme uptake. There was no study that documented on determinants of enrollment in CBHI in Ethiopia in general and in South Gondar Zone in particular.

Research Design

A community primarily based cross sectional study design was used. The study website is found in South Gondar Zone in Amhara region, 613 Km from Addis Ababa, Ethiopia. The whole population of the Zone is calculated at 2,051,738(1,041,061 male and 1,010,677 female). There are 15 rural districts & 5 city administrations in South Gondar Zone. Concerning to health service institutions; there are one governmental referral hospital and 12 primary hospitals,73 health centers, 76 personal health facilities (hospitals & better clinics) and 145 health posts. A community primary based cross sectional study was conducted notably in rural Kebeles (the smallest social unit in Ethiopia) in April 2020.

Population of the Study & Methods of Data Collection

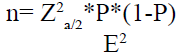

Household heads who were residents (lived for quite 6 months within the Kebeles) of the chosen districts were included. The sample size determined exploitation the only population proportion formula by assumptive a 58 proportion (Table 1) based on the 2015 the Ethiopian insurance agency pilot study, that according that 58 % of the households within the study space were members of the scheme), a 5% margin of error, a 95% confidence level, and 5% non-response rate.

| Variables | Description | Frequency n (%) |

|---|---|---|

| Sex | Male | 897 (88.5) |

| Female | 117 (11.5) | |

| Age | Less than 39 years | 330 (32.5) |

| 40-49 years | 318(31.4) | |

| 50-59 years | 256(25.2) | |

| 60 years above | 111(10.9) | |

| Marital status | Married | 873 (86.1) |

| Single | 27 (2.7) | |

| Divorced | 114 (11.2) | |

| Education | Unable to read & write | 144 (14.2) |

| Able to read & write | 437(43.1) | |

| Primary school | 332(32.7) | |

| Secondary school & above | 101(10) | |

| Occupation | Farmers | 960(94.7) |

| Merchants | 9(0.85) | |

| Daily laborers | 19 (1.84) | |

| Housewife | 3(0.3) | |

| Others | 23(2.31) | |

| Family size | < 2 members | 217(21.4) |

| 3-4 members | 568(56) | |

| 5-7 members | 186(18.3) | |

| > 7members | 44(4.3) | |

| Family wealth | Very poor | 328 (32.3) |

| Poor | 309 (30.5) | |

| Rich | 297 (29.3) | |

| Very rich | 78 (7.7) |

Table 1: Demographic characteristics of respondents.

A total 1,035 family heads participated within the study. A time period sampling procedure was wont to choose participants. Firstly 3 of the 13 CBHI implementing districts were arbitrarily handpicked. Secondly, 9 Kebeles were arbitrarily hand-picked out of the 3 districts (Fogera, Farta & Laye-Gayent). Thirdly, house heads were hand –picked by the systematic sampling technique from every Kebele [12].

A cross sectional survey was dole out by employing a semi-structured form to assemble knowledge from hand-picked representative households within the Zone. The first knowledge was collected via associate enumerator –administered queries that comprised, among others things, house characteristics, theme connected factors, the profit package style, social capital, institutional and provide aspect factors that are thought about to be vital variables poignant house CBHI enrollment.

The instrument was written in English and translated to Amharic and back to English by language specialists. Besides, to take care of its consistency, the form was pre-tested on native individuals living outside the chosen Kebeles and Cronbach’s alpha average value of variables was done.Epi-info version 3.5 was used for data entry [11]. Descriptive statistics, like frequency distributions, tables, graphs were wont to gift the characteristics of the data. Bi-variable analysis was performed to assess the strength of association of the independent variables with the variable and every one the variables were fitted for the statistical method. The results of the many freelance variables on CBHI enrollment call were assessed through the multi-variable analysis and a STATA 10 statistical package was used for the logistic regression model.

To estimate the strength of association between the freelance variables and also the CBHI enrollment odds ratio, a 95% CI and p-values were used [13].

Besides, totally different diagnostics tests were done, notably goodness of match of the model by the Hosmer and Lemeshow tests; where (where p-value of 0.0792 was found), Variance inflation issue (VII) for the multiple regression check (the mean VII result was 1.49) and sample size sufficiency check was additionally done to increase accuracy and manage unsupportive effects as logistical regression can manage numerous confounders for big sample size [14].

The number of individuals enclosed within the multiple logistical regressions was 1,014 with a missing value of 2.3 that was treated through the imputation technique [15,16] (using mean value for a continuous variables and mode for categorical variables).

Operational Definition of Variables

The scale and measuring for many of the variables utilized in this study were tailored from the federal Insurance Agency of Ethiopia pilot study 2017. However, variables like wealth and social capital were taken from EDHS 2011 and international Bank group respectively.

A. CBHI awareness: This refers to house heads data for CBHI existence, its principles and significance. It had been assessed by asking the participants 5 sets of connected queries. The Cronbach’s alpha value was .822.

B. Benefit package: Refers to the sufficiency of health services that are offered by the theme that might be lined through out of pocket payment at times of sickness; and the premium amount charged. This was measured by two questions using the four Likert scale questions with a Cronbach’s alpha value of .773.

C. Quality of service delivery: This includes health workers perspective, handiness of medicine, facilities (medical instrumentality, waiting time, and also the rate of treatment’s results of the health service provider, and measured via five Likert scale kind questionnaires. The cronbach’s alpha result of this variable was .83.

D. Scheme connected factors: Refer to transparency on theme rules, regulation and procedures measured through four Likert scale kind question with a Cronbach’s alpha value of .884.

E. Institutional factors: Include regulative mechanisms, criticism handling systems and insurance education. This variable was measured by five Likert scale kind quetions. The Cronbach’s alpha result of this variable was .788.

F. Supply aspect factors: To the standard of care and distance the household’s homes from the closest hospice that is measured by four Likert scale kind queries with a Cronbach’s alpha value of .886.

G. Social capital: Includes trust, networks, involution, social norms, and commonality & closeness are features of the system the community. Five Likert scale kind of queries were adopted from the World Bank cluster to live the variable with Cronbach’s alpha value of .756.

H. Wealth: Refers to household and was measured by queries adopted from EDHS 2011. Principal elements analysis in STATA was wont to develop the index.

Acknowledgments

First we would like to thank all study participants for their cooperation in providing the necessary information. We would also thank data collectors and supervisors for the devotion and quality work during data collection period.

Authors’ Contributions

The first initiations of this research title were credited to the first author, AlebelWoretaw. To the rest of the tasks, like study design, data collection, oversight, data interpretation, and manuscript writing all authors contributed equally. All authors have read and approved the manuscript.

Competing interests: No authors have competing interests.

Source: Own survey, 2020

A total of 1,035 household heads with 98% response rate participated within the study. Of the participants, 117 (11.5%) female & 897 (88.5%) were male with a mean age of 46.2 (± 14.02).

The large amount of respondents were Orthodox Christian by religion and married the majority of respondents were farmers, a mean family size was 6.78 (± 4.54). 43.1% were able to read and write and also the household wealth of 32.3% & 30.5% of the respondents were in the first class of lowest wealth.

Factors Related To Cbhi Enrollment

The outcome variable (CBHI enrollment decision) was treated as binary: “1” for enrolled and “0” for un-enrolled within the economics model. The econometrics logistic analysis showed that household family size was significantly associated with CBHI enrollment.

As the household size increased by one unit, the likelihood to join the scheme increased by 2.18 times (AOR =2.18; CI = 1.13–1.45). Likewise, participants with good CBHI awareness were 4.78 times more likely to join the scheme compared with their counterpart (AOR = 4.78; CI = 1.75–15.7).

The results also indicated that household with good perceived family health status were 0.59 times less likely to enroll compared with those with poor family health (AOR = .590; CI = .281–.906). Similarly, household who had family members with chronic disease were 4.42 times more likely to join compared with their counterparts (AOR = 4.42; CI = 1.92–8.22).

In the study, scheme benefit package adequacy indicated a strong positive effect on enrollment. Household which perceived that the benefit package of the scheme was adequate were 3.18 times more likely to enroll compared with those who perceived inadequate benefit (AOR=3.18; CI=1.90-6.20).

The results also revealed that respondents with good perception about the quality of health services were 4.69 times more likely to enroll in CBHI than respondents who perceived low health service quality (AOR = 4.69; CI = 1.78–7.70). Besides, households in the fourth very richest were 4.52 times more likely to enroll than the poorest in the first quintile (AOR = 4.52; CI = 1.78–7.94).

In the social capital dimension solidarity was strongly associated with enrollment. Household who believed existence of good community solidarity were 4.87 times more likely to join than those who responded existence of weak community solidarity (AOR = 4.87; CI = 2.06–6.93).

In this study, the CBHI enrollment rate of South Gondar Zone was 68.17%. Consistent with the regression analysis, family size, health standing of a family, and chronic sickness within the social unit, theme service adequacy, community commonness, health establishment’s service quality, CBHI awareness and wealth were important determinants of households CBHI enrollment. What is more, the study indicated proof of adverse choices. Therefore, in-depth and property awareness creation programs on the theme, stratified premium supported the economic standing of households, incorporation of social capital factors, notably community commonness within the theme implementation area unit very important to reinforce property enrollment. Moreover, as family health standing and chronic disease were important determinants of enrollment. The government may have seemed for choices to form the theme necessary.

Citation: Asaye AW, Engidaw MT (2021) Determinants of Community Based Health Insurance Implementation: Evidence from South Gondar Zone, Amhara Region (2020). J Women's Health Care 10:528.

Received: 27-Mar-2021 Accepted: 23-Apr-2021 Published: 30-Apr-2021 , DOI: 10.35248/2167-0420.21.10.528

Copyright: ©2021 Asaye AW, et al. This is an open-access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.