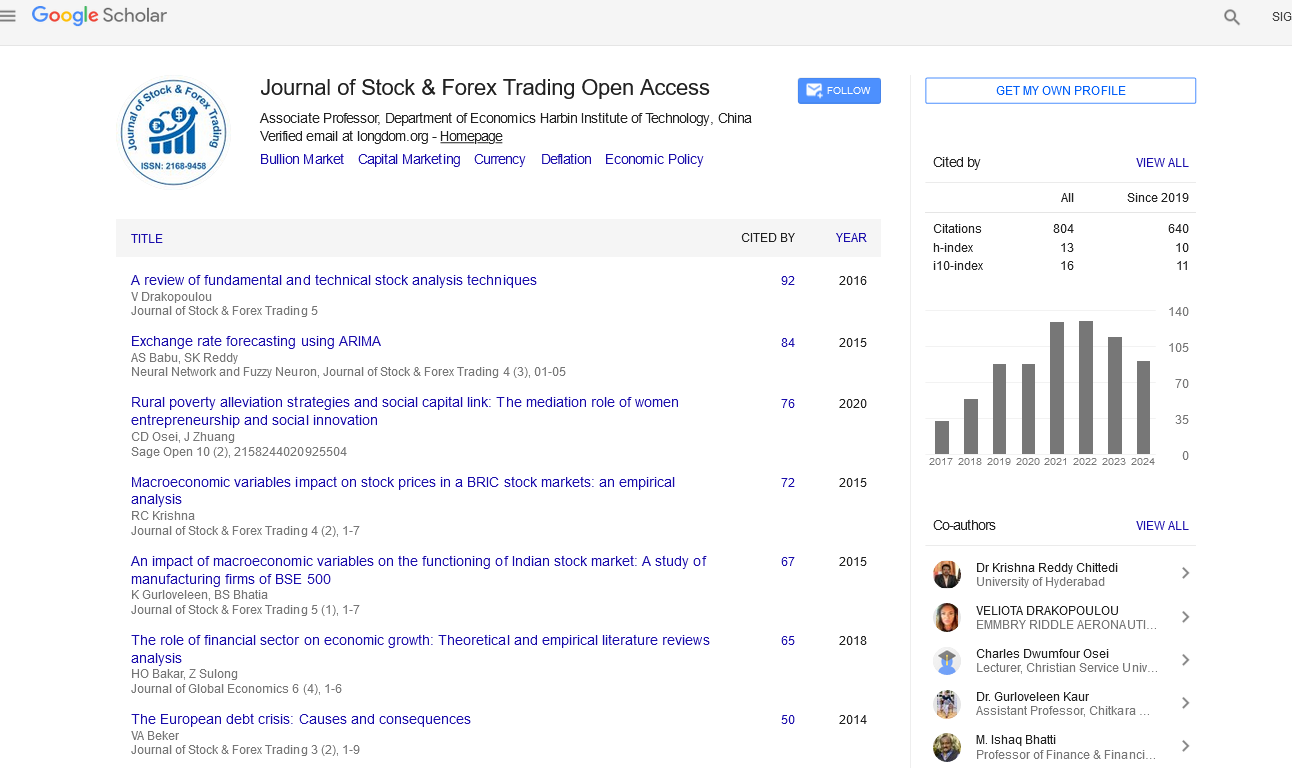

Journal of Stock & Forex Trading : Citations & Metrics Report

Articles published in Journal of Stock & Forex Trading have been cited by esteemed scholars and scientists all around the world. Journal of Stock & Forex Trading has got h-index 13, which means every article in Journal of Stock & Forex Trading has got 13 average citations.

Following are the list of articles that have cited the articles published in Journal of Stock & Forex Trading.

| 2024 | 2023 | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | 2013 | 2012 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Total published articles |

28 | 32 | 20 | 23 | 28 | 7 | 6 | 0 | 13 | 21 | 33 | 12 | 17 |

Research, Review articles and Editorials |

4 | 9 | 5 | 0 | 0 | 7 | 5 | 0 | 10 | 16 | 25 | 12 | 17 |

Research communications, Review communications, Editorial communications, Case reports and Commentary |

12 | 23 | 15 | 0 | 0 | 0 | 1 | 0 | 1 | 54 | 8 | 0 | 0 |

Conference proceedings |

0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

Citations received as per Google Scholar, other indexing platforms and portals |

107 | 113 | 132 | 129 | 89 | 88 | 54 | 33 | 40 | 18 | 6 | 0 | 0 |

| Journal total citations count | 813 |

| Journal impact factor | 5.58 |

| Journal 5 years impact factor | 5.03 |

| Journal cite score | 5.02 |

| Journal h-index | 13 |

| Journal h-index since 2019 | 11 |

Important citations (371)

Srivastva, marinalini, and gagandeep sharma. "risk and return linkages among stock markets of selected asian countries." tsme journal of management 6.1&2 (2016): 1-16. |

|

???????? ??? ?? ?? ? ??????. "??? ??? ??????? ????? ?????????? ???? ????." thai science and technology journal (2020): 26-40. |

|

???????, ?. ?. "???????????? ???????? ????????-????? ??? ????????????? ????????? ????????? ???????." ????????? ? ????????????? 1 (2018): 98-110. |

|

Ibrahim, umar abbas, and aisha muazu. "effect of bureau de change establishment on the stability of exchange rates in nigeria." (2020). |

|

Joshi, vikram k., et al. "modeling exchange rate in india–empirical analysis using arima model." |

|

Xing, shikai, zhongliang guan, and laisong kang. "a maturity model for examination management in university." 2018 8th international conference on logistics, informatics and service sciences (liss). ieee, 2018. |

|

Maneejuk, paravee, and wilawan srichaikul. "forecasting foreign exchange markets: further evidence using machine learning models." soft computing 25.12 (2021): 7887-7898. |

|

Mansour, fatma, murat can yüksel, and mehmet fatih akay. "predicting exchange rate by using time series multilayer perceptron." |

|

Salehi, mahdi, and nastaran dehnavi. "audit report forecast: an application of nonlinear grey bernoulli model." grey systems: theory and application (2018). |

|

Xiu-rong, chen, and tian yi-xiang. "rbf model based on the improved kele algorithm." |

|

Tepdang, sayan, and ratthakorn ponprasert. "forecast of changes in exchange rate between thai baht and us dollar using data mining technique." snru journal of science and technology 12.3 (2020): 213-221. |

|

Behera, himansu sekhar. "towards designing and performance analysis of evolving higher order neural networks for modeling and forecasting exchange rate time series data." proceedings of icetit 2019: emerging trends in information technology 605 (2019): 258. |

|

Mammadov, z., n. mirzaliyev, and f. tuzcuoglu. "forecasting exchange rate series using box-jenkins methodology." (2021). |

|

Kanat, ersin, and ?ener dilek. "pay sened? f?yatlarinin bulanik mantik yakla?imi ?le tahm?n ed?lmes?: b?st sanay? f?rmalari Üzer?ne b?r ara?tirma." uluslararas? yönetim ?ktisat ve ??letme dergisi 14.4 (2018): 977-1002. |

|

Isiaka, abdulaleem, abdulqudus isiaka, and abdulqadir isiaka. "forecasting with arma models: a case study of the exchange rate between the us dollar and a unit of the british pound." international journal of research in business and social science (2147-4478) 10.1 (2021): 205-234. |

|

Chin, kuo-hsuan, nhan nguyen-thanh, and cong-duc tran. "stock indices forecast by hybrid model from garch families: evidence from global markets." journal of accounting, finance & management strategy 16.1 (2021). |

|

Toledo, nhoriel i. "the autoregressive integrated moving average model in forecasting philippine peso-united states dollar exchange rates." journal of physics: conference series. vol. 1936. no. 1. iop publishing, 2021. |

|

?or?evi?, marina, jadranka ?urovi? todorovi?, and milica risti?. "improving performance of vat system in developing eu countries: estimating the determinants of the ratio c-efficiency in the period 1997-2017." facta universitatis, series: economics and organization (2019): 239-254. |

|

Kamal, rasti shirzad. sensitivity analysis of change of currency exchange arima modeling parameters between (0, 1, 1) and (1, 1, 0) depending on economic policies. ms thesis. eastern mediterranean university (emu)-do?u akdeniz Üniversitesi (daÜ), 2019. |

|

Escudero, pedro, willian alcocer, and jenny paredes. "recurrent neural networks and arima models for euro/dollar exchange rate forecasting." applied sciences 11.12 (2021): 5658. |

|